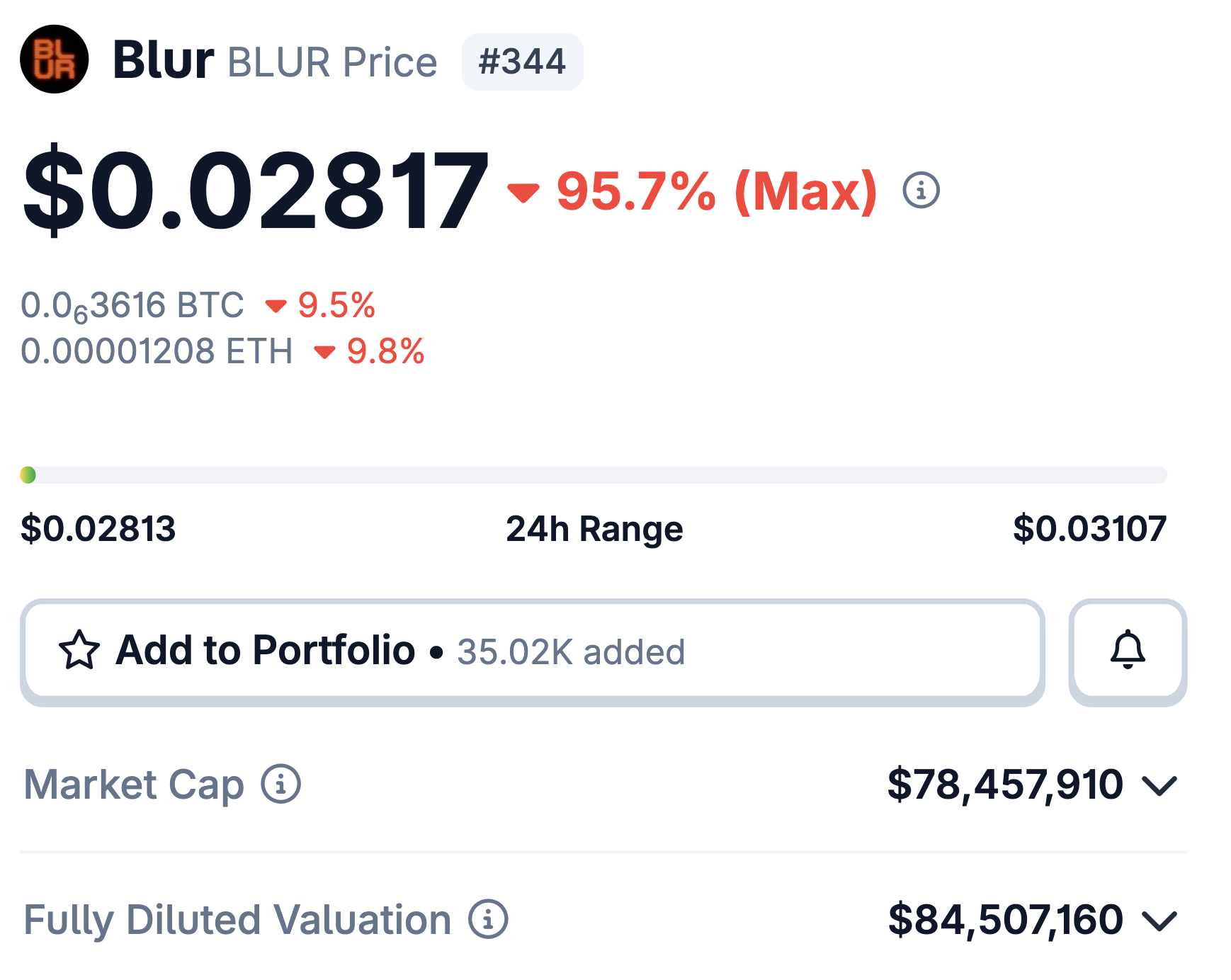

$BLUR price. Source: CoinGecko. April 26, 2026.

Diligence Research is long $BLUR.1

April 2026

The market has written off $BLUR as an abandoned NFT marketplace token. We traced the infrastructure and found an active private beta for a new product: trench.com, a memecoin trading terminal built on Blur's infrastructure. We believe this is a new product line under $BLUR, not a separate project. In our view, $BLUR is mispriced as a dead project when the team is actively shipping into a proven, high-revenue crypto vertical and nearing public launch.

The case for $BLUR being dead is easy to make. The official @blur_io account has tweeted twice in the last twelve months. Its founder @PacmanBlur, four. The last meaningful product update was Blend, launched in May 2023 - three years ago. The token trades at $0.0282, market cap ~$78M, down 95.7% from peak.

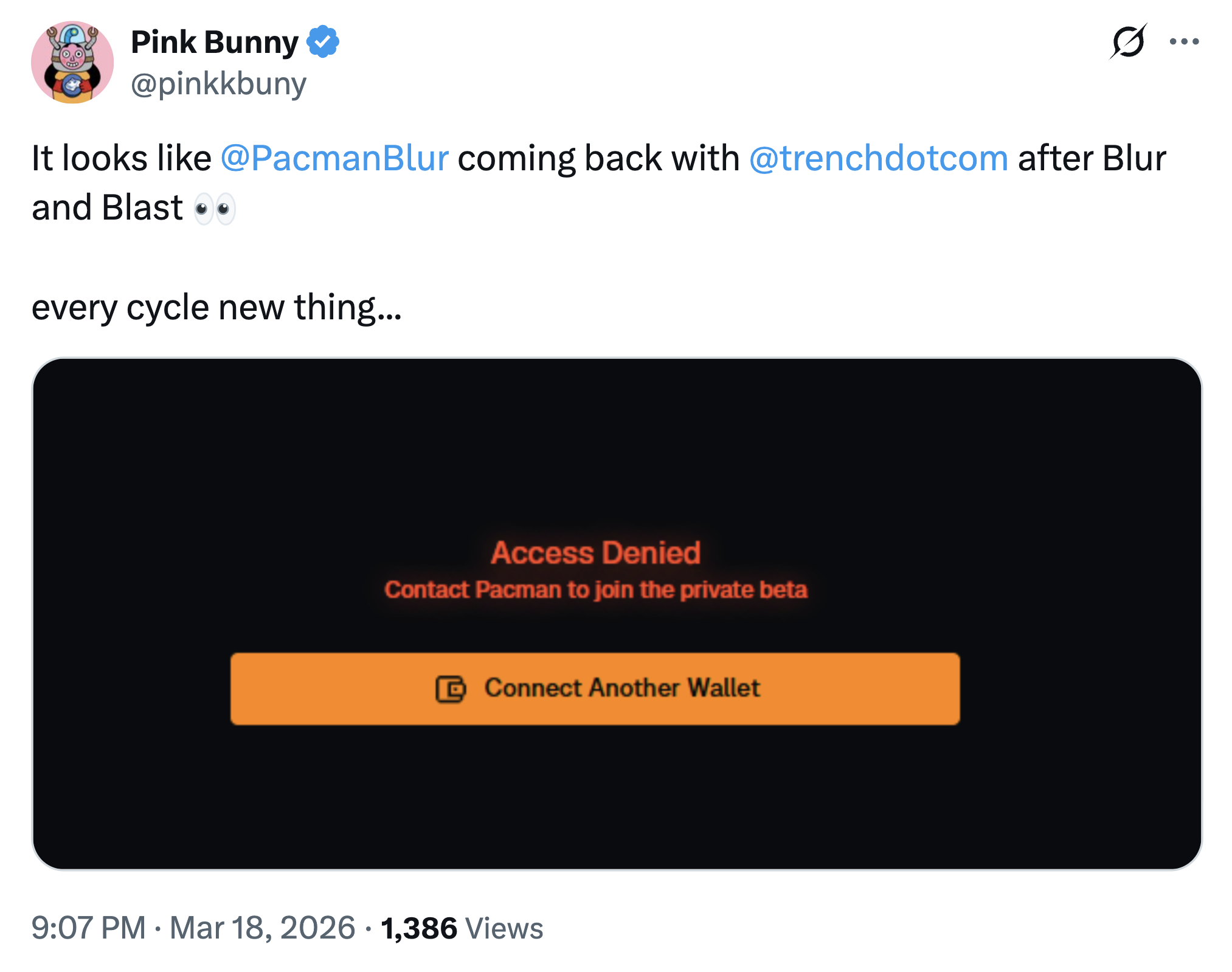

In March 2026, @pinkkbuny tweeted:

Three weeks later, Pacman tweeted that he was not raising money for a new project. In the replies, @ericzalusky asked whether @trenchdotcom was his. He did not respond to the question.

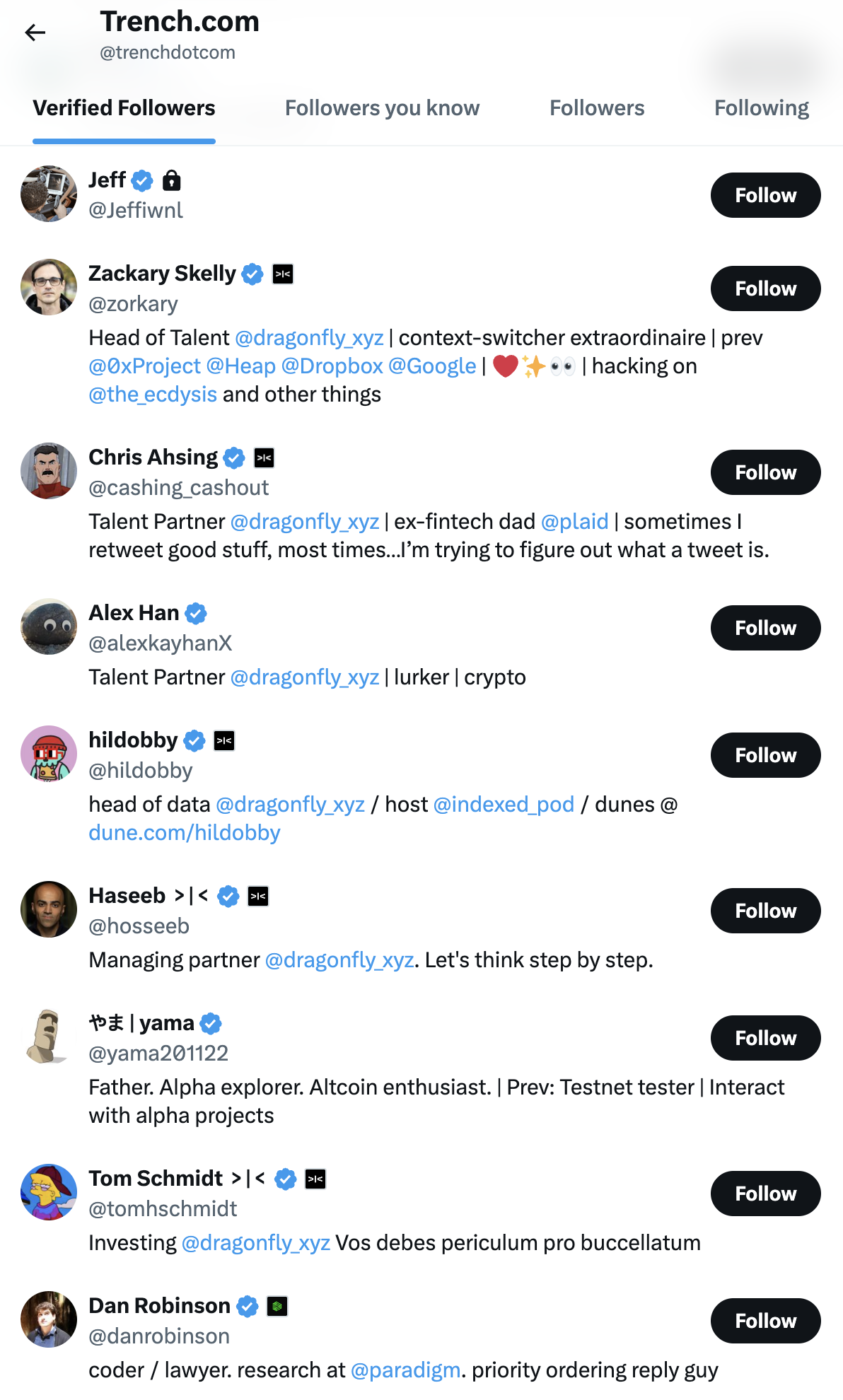

The @trenchdotcom X account was created in December 2025. It has made zero tweets. It follows zero accounts.

According to @supraEVM, Pacman was the first follower of @trenchdotcom:

Its follower list is also notable:

From Dragonfly Capital: Haseeb Qureshi, Tom Schmidt, hildobby, Chris Ahsing, Zackary Skelly, and Alex Han. From Paradigm: Dan Robinson. Both firms are investors in Blur and Blast.

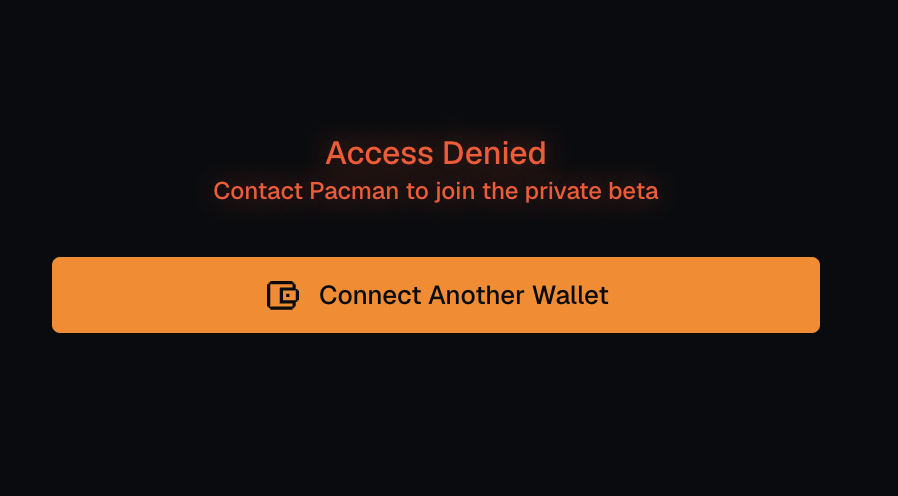

We visited trench.com and attempted to log in:

The site names Pacman, and Pacman follows @trenchdotcom on X. The link runs both ways.

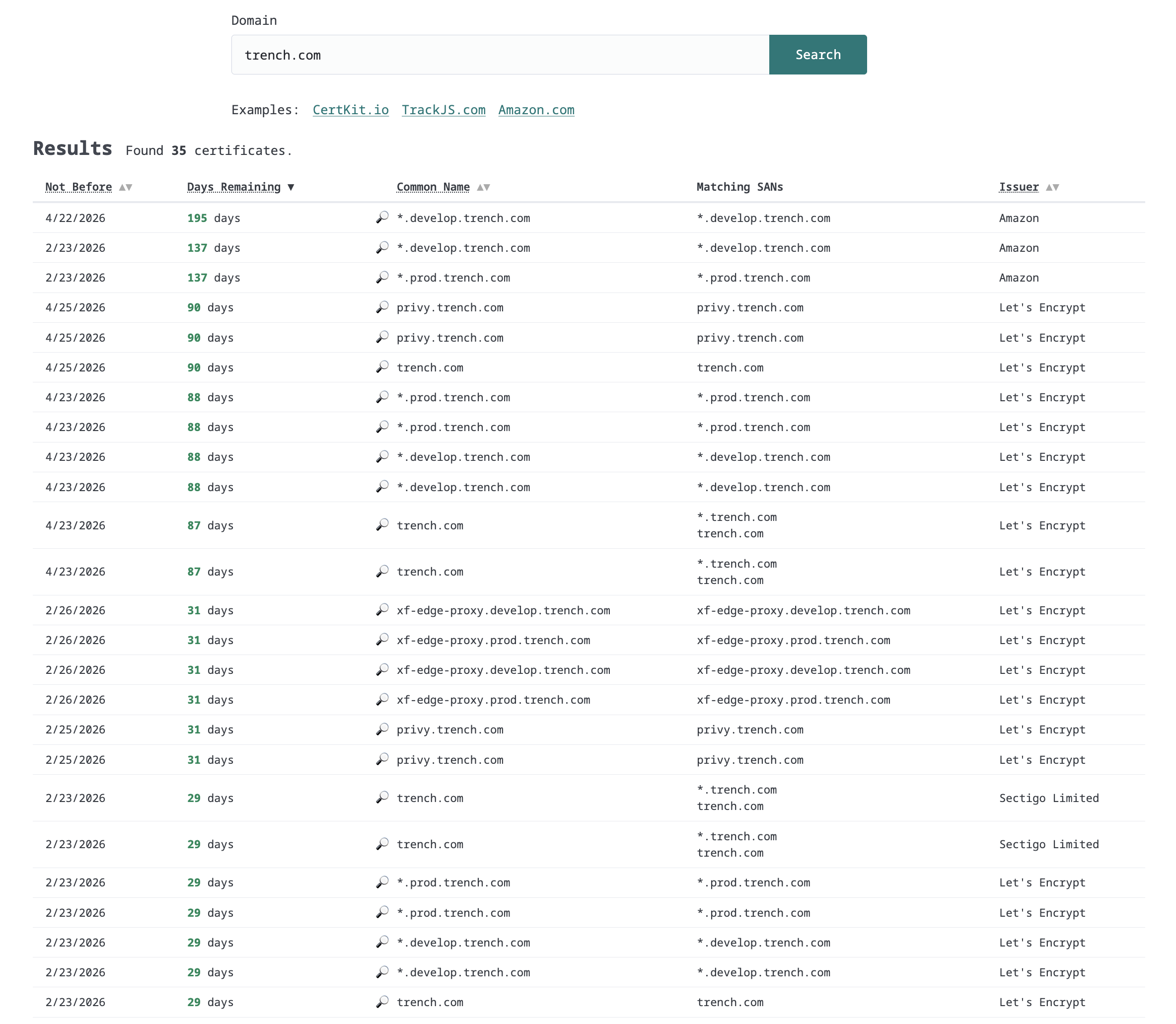

With the Pacman-Trench connection established, we pulled the SSL certificate transparency logs for all three of Pacman's projects: trench.com, blur.io, and blast.io.

Certificate transparency logs for trench.com show recent SSL certificates for development, production, and authentication subdomains:

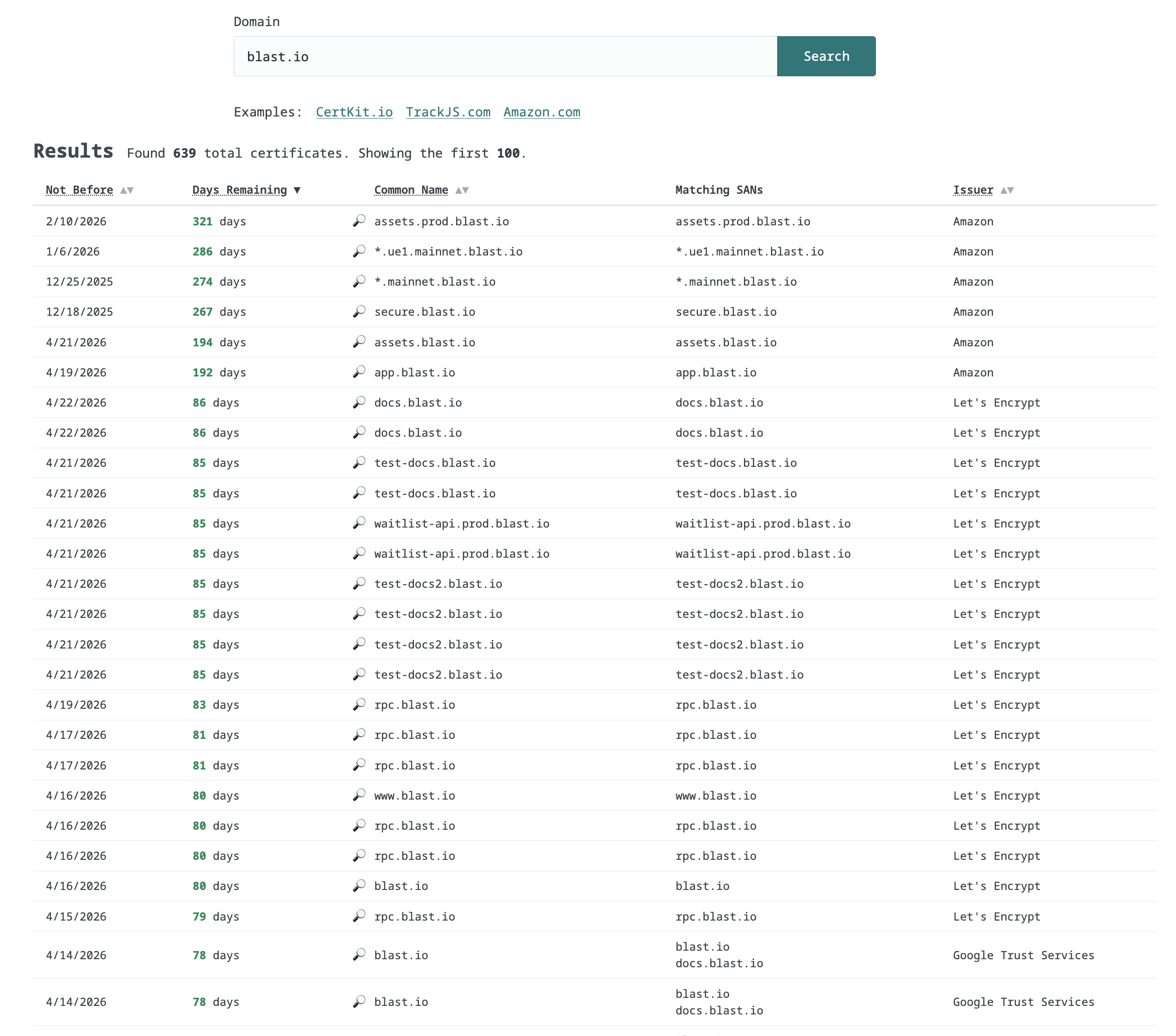

We then pulled the certificate logs for blur.io. The subdomain patterns matched:

For comparison, blast.io's certificate logs show no xf-edge-proxy or privy subdomains:

Three subdomain patterns are shared between trench.com and blur.io, but not blast.io:

| Pattern | trench.com | blur.io | blast.io |

|---|---|---|---|

xf-edge-proxy.prod.* | Yes | Yes | No |

xf-edge-proxy.develop.* | Yes | Yes | No |

privy.* | Yes | Yes | No |

While the matching infrastructure provides circumstantial evidence of a link between trench.com and blur.io, it is not conclusive on its own.

We visited every subdomain across the cert logs for all three domains. Most resolved to standard infrastructure. But trade.blur.io - surfaced by the privy.trade.blur.io certificate - redirected to trench.com and asked us to connect with a Phantom wallet.

We believe trench.com is a memecoin trading terminal. The name is a tell - "the trenches" is slang for memecoin trading.

The privy.trench.com and privy.trade.blur.io subdomains in the certificate logs above point to a trading product. Privy lets users trade in one click, without wallet popups or gas confirmations. Axiom, the current market leader, uses Turnkey - a competing wallet infrastructure provider - for the same purpose. Blur's NFT marketplace has never used Privy. A trading terminal would.

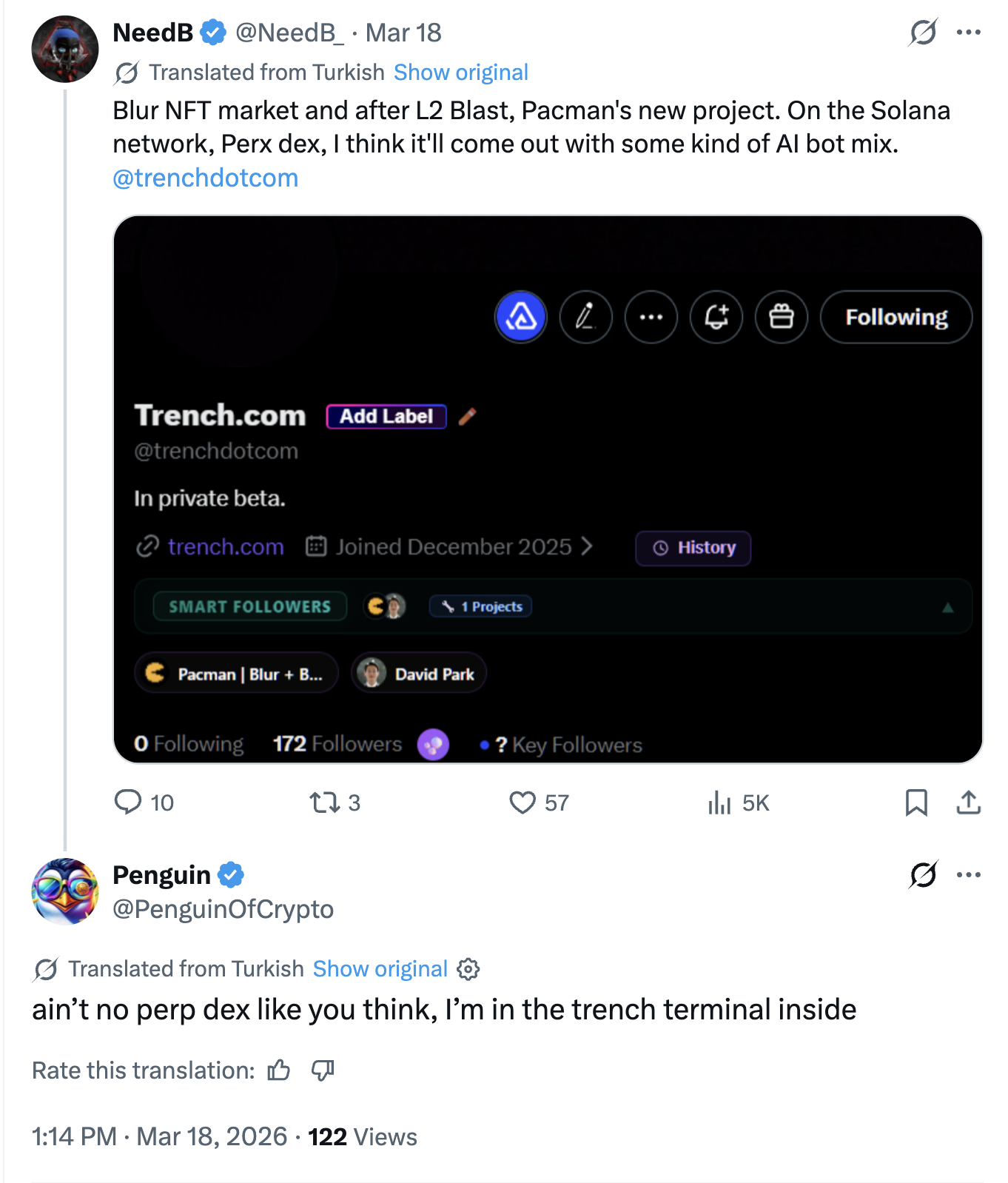

@PenguinOfCrypto, a beta user, replied that he was "in the trench terminal inside" - not a perp DEX as some had speculated.

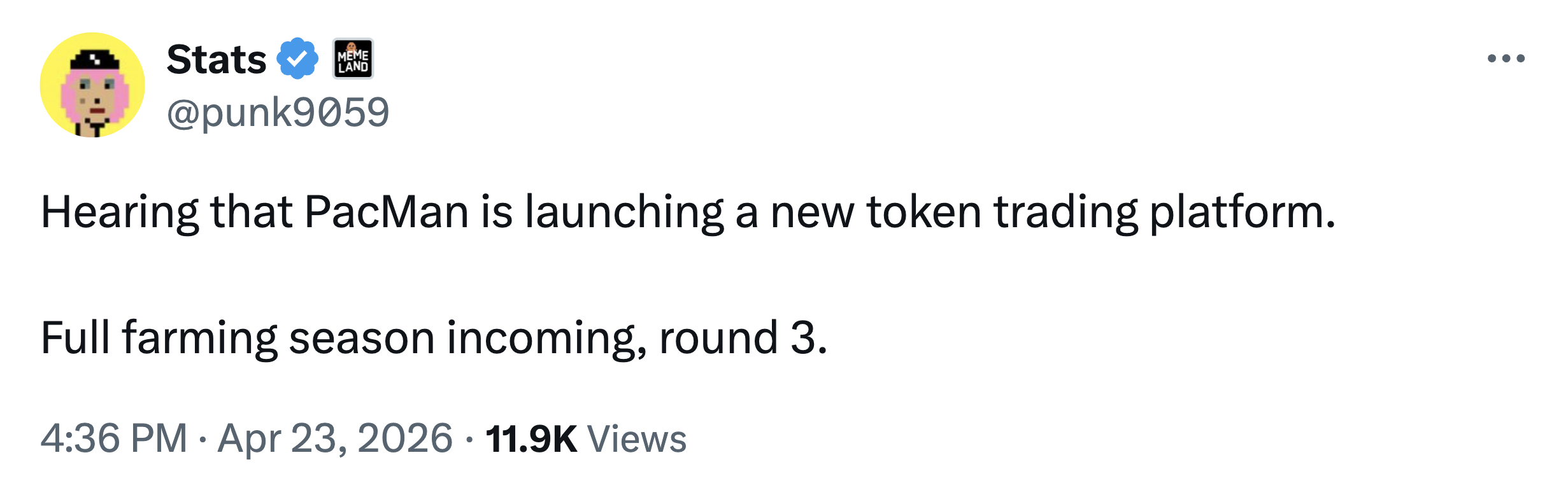

On April 23, @punk9059 tweeted that he was hearing Pacman is launching a new token trading platform. He added: "full farming season incoming, round 3."

We believe trench.com is a Blur product suite with a separate domain - not a new project, and not a candidate for its own token launch. In our view, there is no "wait for $TRENCH." $BLUR is the most direct exposure.

The infrastructure points to trench.com being a Blur product:

The incentive structure rules out a separate token:

If trench.com must sit under one of Pacman's two existing projects, the evidence points to Blur.

The evidence suggests trench.com is approaching public launch.

Production SSL certificates for trench.com have been active since early 2026. The private beta is live, with access gated behind wallet connection. A person familiar with the product told us a referral program has been added. Referral programs typically appear in the final stages before public launch.

Scope note. This report does not model macro NFT-cycle dynamics. We are aware attention has rotated back into NFTs recently, with calls that now is the right window for an OpenSea TGE. These are outside the scope of this analysis. The valuation below prices the trench.com catalyst alone; macro tailwind, if it materializes, is upside not modeled.

We separate our analysis into two parts: the base case, which requires only accepting the evidence presented in this report, and the speculative upside, which requires assumptions about trench.com's market success and $BLUR tokenomics.

This case requires only one thing: the market recognizing that the team behind $BLUR is not dead - that it is building a product in one of crypto's highest-revenue verticals, with a launch in sight.

$BLUR is priced at ~$78M as if the team has abandoned the project. There are no clean analogues for a "dead-to-alive" repricing in crypto - it rarely happens. The closest we found are PENDLE (2.2x in 30 days after connecting to the EigenLayer restaking meta in January 2024) and IMX (2x in 30 days after announcing its AWS partnership in October 2023). Neither is a tight fit: both involved teams that were visibly active, not presumed dead, and both repriced despite activity already being partially priced in. We discount accordingly, applying a 1.3-2x range rather than the 2x+ those tokens saw, implying $101-156 million. $BLUR has zero activity priced in.

Three factors make this repricing asymmetric:

Everything below this line requires assumptions about trench.com's execution and $BLUR's tokenomics. We present it as upside scenarios, not base case.

Market sizing. Axiom, the current market leader, generated $370 million in cumulative revenue over twelve months. At peak, $62.5 million in a single month (May 2025). The market has since cooled: Axiom's current annualized revenue is ~$78 million. At ~57% market share, this implies a total Solana terminal market of ~$137 million annualized.

As of April 26, 2026, $BLUR traded at ~$78M with no trench.com revenue priced in. In the scenarios below, we treat trench.com's value as additive to the current market cap.

Using @thedefiedge's analysis of P/S ratios across revenue-generating protocols, the closest comparable sectors for trench.com are DEXs (median 10.1x) and launchpads (median 13.4x). We use a conservative 10x multiple. The scenarios below represent our opinion of what $BLUR could be worth under different assumptions. They are not price targets or predictions of market behavior.

| Scenario | Market Size | Market Share | Ann. Revenue | Value Add | Implied FDV | Upside |

|---|---|---|---|---|---|---|

| Bear | $68M | 3% | $2.0M | $20M | $98M | 1.3x |

| Conservative | $137M | 3% | $4.1M | $41M | $119M | 1.5x |

| Optimistic | $137M | 7% | $9.6M | $96M | $174M | 2.2x |

| Bull | $137M | 10% | $13.7M | $137M | $215M | 2.8x |

| Bull (market recovery) | $275M | 10% | $27.5M | $275M | $353M | 4.5x |

| Blue sky | $500M+ | 20% | $100M+ | $1B+ | $1B+ | 13x+ |

Implied FDV = current $78M FDV + Value Add. These scenarios model trench.com generating revenue. If trench.com fails to launch materially, only the base case narrative repricing applies.

Additional optionality. Everything below is speculation. None of it is required for the base case or the scenarios above. But $BLUR has structural positioning that no competitor currently matches.

$BLUR can be the only meaningful token in the trading terminal space. Axiom, Photon, BullX, and GMGN have not launched tokens and show no signs of doing so. They are printing hundreds of millions in fees without having to share value with users - there is no incentive to change that by launching a token. We believe it is unlikely these incumbents would seriously consider doing so unless a token-enabled competitor like trench.com becomes a large enough threat to force their hand. Until then, $BLUR may be the only liquid vehicle for exposure to the trading terminal thesis.

Airdrop war chest. Blur allocated 51% of total supply (1.53 billion $BLUR) to the community, split between 12% (360 million) for the Season 1 airdrop and 39% (~1.17 billion) for the community treasury. Only 660 million $BLUR has ever been distributed - all of it via Seasons 1 and 2. Seasons 3 and 4 switched entirely to $BLAST rewards, with no additional $BLUR airdropped since. Up to 870 million $BLUR (~29% of total supply, ~$25 million at current prices) remains available, subject to the original four-year vesting schedule, with daily unlocks continuing through early 2027.

This treasury could be deployed for an airdrop season aimed at attracting traders to trench.com. Blur pioneered the points system that became the industry standard - it is how the NFT marketplace took market share from OpenSea, and the same team would be running it again. If trench.com launches with an airdrop program, it creates the potential for a flywheel: airdrop incentives attract traders, usage drives token demand, a rising token price increases the dollar value of the remaining treasury, funding further incentives.

Buyback optionality. Fee-based token buybacks have become an increasingly standard tokenomics mechanism since Blur launched three years ago - Hyperliquid, Jupiter, Raydium, and Pump all implement revenue-to-buyback programs. This pattern was not widespread when $BLUR's tokenomics were designed. We have no evidence that Blur plans to implement buybacks using trench.com revenue. But if the dominant pattern of 2025-2026 is applied, $BLUR would be the first major trading terminal token with direct value accrual.

"Axiom has 57% market share. Why would trench.com win?"

Blur took NFT marketplace share from a dominant, better-resourced OpenSea. The team won on UX. The December 2025 hiring post for "low latency trading systems" suggests the same engineering rigor at trench.com.

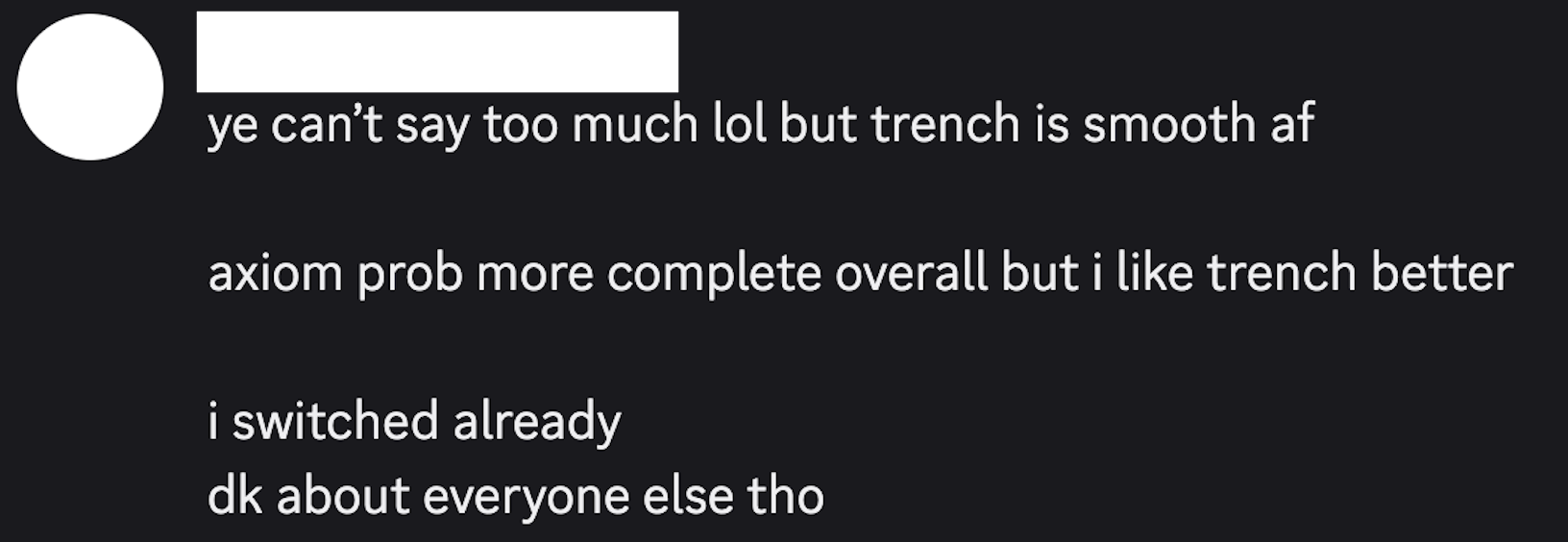

The same source described trench.com as "smooth" compared to Axiom.

"The memecoin terminal market is declining."

It is. Axiom's revenue is ~90% off its peak. We model this with scenarios from bear to blue sky. The base case does not require a market recovery, only that the market recognize the team is alive - a 1.3-2x repricing consistent with comparable catalysts.

"Pacman's reputation is tarnished."

Every major trading terminal extracts hundreds of millions in fees without redistributing value, leveling the reputational playing field. Pacman is polarizing, but also one of crypto's most recognized names. When trench.com launches, it will not struggle for attention.

In practice, the reputational discount has limits. Replying to the rumor, even a Pacman skeptic argued a guaranteed airdrop "instantly puts the platform ahead of axiom, photon etc."

The grievance creates demand for an airdrop-funded entrant. Pacman's reputation does not erase that demand. At minimum, this means substitution toward trench. The stronger case is strategic: if the grievance coalesces into a coordinated rally using trench.com as the lever to force incumbents into airdrops, incumbents face a binary - airdrop, or cede ground. Both responses strengthen trench's positioning.

This is the playbook Blur ran against OpenSea: airdrop-funded points, trader rally, incumbent forced to match or cede ground. Pacman has done this before.

OpenSea ceded ground first. The match came late. Whether Axiom plays it differently is the open question.

As of April 26, 2026, trade.blur.io redirected to trench.com. The infrastructure patterns match. The team was hiring for trading terminal engineering while the NFT marketplace sat idle. The private beta is active and, based on what we have seen, launch appears close.

The market still prices $BLUR at $78M as if the team has quit. In our view, it has not priced in what is coming.

We are long $BLUR.

Disclaimer

This report has been prepared and published by Diligence Research ("Diligence Research" or "we" or "us"). Diligence Research is an online research publication that produces due diligence-based reports on publicly traded digital assets. This report is the property of Diligence Research.

As of the time and date of this report, Diligence Research holds a long position in $BLUR (the "Covered Asset"), including spot tokens and/or derivatives linked to the Covered Asset. Upon publication, we may increase, decrease, or close our position at any time without notice. Changes in our position are not a reflection of a lack of conviction in our thesis; they reflect routine portfolio and risk management.

We are a "for profit" research organization with a non-traditional revenue model - rather than accepting advertising or subscriptions, we finance our research through taking positions in the digital assets on which we report. This revenue model enables us to report in depth on a limited number of investigations, and also entails taking significant financial risk. In order to manage that risk, we must adjust open positions as we deem prudent. We do not provide price targets. We may express our opinion of what a digital asset is worth, but an opinion of value differs from a price target in that we do not purport to predict how the market as a whole might value a digital asset. We therefore do not hold positions until they reach any stated valuation.

We are not providing you with a recommendation to buy or sell the Covered Asset or any other digital asset. We are articulating our reasons for holding a position at the time of publication. We do not provide investment advice.

We have no duty or obligation to update this report or to inform you of any changes in the size or direction of our position. All information and opinions set forth herein are for informational purposes only. Under no circumstances should any information or opinions herein be construed as investment advice, as an offer to sell, or the solicitation of an offer to buy any digital asset or other financial instrument.

This report represents the views of Diligence Research only. To the best of our knowledge, all information contained herein is accurate and reliable and has been obtained from publicly available sources that we believe to be accurate and reliable, and in some cases from individuals who have shared their observations with us. The information presented herein is "as is," without warranty of any kind, whether express or implied. This report contains a large measure of analysis and opinion. All expressions of opinion are subject to change without notice.

This report is opinion journalism. We are providing our journalistic opinions about issues of interest to the general public. Before making any investment decision, you should conduct your own research and due diligence.

Digital assets are highly volatile and speculative. Trading and investing in digital assets involves substantial risk of loss. Past performance is not indicative of future results. You should never invest more than you can afford to lose.

By viewing or accessing this report, you agree to the following:

You agree that your use of this report is at your own risk.

Diligence Research shall not be liable for any claims, losses, costs, or damages of any kind, including direct, indirect, punitive, exemplary, incidental, special, or consequential damages, arising out of or in any way connected with this report. This limitation of liability applies regardless of any negligence or gross negligence of Diligence Research. You accept all risks in relying on the information and opinions herein.

You agree and understand that, by the time you read this report, we may have already increased, decreased, or closed our position in the Covered Asset, and we are under no obligation to disclose subsequent changes. You should not make any investment decision based on your interpreted view of our positioning.

You agree that any dispute arising from or related to this report shall be governed by the laws of Singapore, and you submit to the exclusive jurisdiction of the courts of Singapore.

The failure of Diligence Research to exercise or enforce any right or provision herein shall not constitute a waiver of such right or provision.

You agree that regardless of any statute or law to the contrary, any claim or cause of action arising out of or related to this report must be filed within one (1) year after the occurrence of the alleged harm that gave rise to such claim or cause of action, or such claim or cause of action be forever barred.

If any provision of these terms is found by a court of competent jurisdiction to be invalid or unenforceable, the remaining provisions shall continue in full force and effect.

The content of this report is the property of Diligence Research and is protected by copyright. You may link to or quote from this report with attribution, but you may not reproduce it in full without written permission.